🔒Diversifying business loans: Lenders and entrepreneurs of color are trying to overcome historic biases and practical barriers in commercial lending

Danielle Spring, owner of Femme Bar in Worcester, hopes to one day move her bar to a larger space to offer separate rooms for dancing and other forms of nightlife. PHOTO ALLAN DINES

Grace Lee emigrated to the U.S. with her family when she was 1 year old.

Grace Lee, CEO and president of St. Mary's Credit Union

While her father had been an engineer in South Korea, he didn’t have enough English proficiency to continue that career in the states. He started off as an airline luggage hand, and when he turned to entrepreneurship, Lee and her sister had to step in.

At eight, nine, and 10, Lee and her sister were translating and negotiating business contracts for their parents.

“We had some really rough moments,” she said.

And it wasn’t just her mom and dad she saw struggling to navigate accessing financing. It was her neighbors, the people at her parish.

“There were cultural obstacles. There were linguistic obstacles. They were just gaps in the process and financial competency in navigating the larger financial institutions,” said Lee. “It's that broader lived experience that I carry with me every day.”

Lee is now president and CEO of St. Mary’s Credit Union in Marlborough, where she began her tenure in August after serving as the Eastern Massachusetts regional president and group lead of New England government banking at Buffalo-based M&T Bank.

Under her leadership, M&T was named the U.S. Small Business Administration Minority Lender of the Year for Massachusetts in 2023 and 2024.

Yet, obtaining business loans for many people of color poses a challenge. On top of historical biases stemming from prejudicial policies like redlining, entrepreneurs of color can often have less familiarity with the financial industry and generally lower credit scores.

“There's an assumption made that they understand how the process works, and when you've been marginalized around access to finances and capital in particular, people don't have a knowledge of how it works,” said Monica Thomas-Bonnick, vice president, business lending officer at Auburn-based Webster Five bank.

Central Massachusetts institutions like Webster Five and St. Mary’s are working to open up the financial system by educating entrepreneurs of color. Culturally-informed, equity-based, and collaborative loaning practices have proven beneficial in Central Massachusetts, for banking institutions and entrepreneurs alike.

Entrepreneurs of color may not have been taught the actual process of obtaining a loan or a business plan, Thomas-Bonnick said. Not everyone knows they need to come to the negotiating table knowing the minutia of what it will cost to run their business.

“Entrepreneurs are dreamers. They have visions, and they focus on that, right? And someone said ‘Go to the bank, and they can give you a loan,’ but no one told them that if you're a startup business, some banks don't lend to startups,” she said.

Trying to get loans

Walking into Femme Bar in Worcester means stepping into a neon pink haze. Nostalgic hits play from the speakers as groups of friends linger around the bar and surround tables into the early hours of the morning.

Femme opened in March 2023 as one of about 30 lesbian bars in the country, but finding financing for the concept was nearly impossible for Danielle Spring and her wife Julie Toupin-Spring. They went to big and small banks and credit unions for business loans, but none of them panned out.

Spring, who is Black, had decided along with Toupin-Spring to put the latter’s name on their applications in an attempt to avoid any racial discrimination in the lending process.

“We really figured putting a white female on everything would help us with everything, but it didn't,” she said. “No one's gonna tell you to your face because you're a woman, or we're not doing this because you're Black. You just know that your business isn't any different than the last business that referred you here.”

They found banks didn’t like to give to restaurants unless the owners had a lot of money behind them, and while SBA does offer loans to restaurateurs, there are a lot of hoops to jump through.

After Spring and her wife struck out at every institution they approached, they ended up using their life savings to launch Femme.

Bernadette Clark, owner of Sharp Designs hair salon

Bernadette Clark, owner of Sharp Designs hair salon in Fitchburg, initially had no luck when applying for SBA loans at various banks. She was told either she didn’t make enough money or her credit wasn’t good enough.

“My credit was outstanding,” she said. “They wouldn't touch me. They just had their noses up. I'm not a white-collar person. I’m sorry.”

Additionally, she was a homeowner with a lot of equity and was even willing to put that on as collateral. In some ways, she felt it was because she is half Black and a single mother.

Eventually, she found the North Central Massachusetts Development Corp., the economic arm of the North Central Massachusetts Chamber of Commerce in Fitchburg, which provides smaller SBA loans to higher-risk applicants.

Before the COVID pandemic, Clark secured a $5,000 loan through NCMDC to allow her to purchase new equipment and supplies as she upgraded her salon and moved it to a larger location. Ever since, NCMDC has supported Clark. Through COVID, the officials there helped connect her to programs and reconfigure loans to keep her business afloat.

“It was tough, scary. But not so scary because I felt as though, if anything goes wrong or something, I could always talk to them and we could always figure something out,” she said.

Systemic biases

One of the main barriers Black and other entrepreneurs of color face when applying for business loans is distrust in the financial system due to previous unpleasant experiences stemming the industry’s history of redlining, said Thomas-Bonnick.

Seven white men came together in 1936 and made a map, commissioned by the Home Owners’ Loan Corp., of Worcester neighborhoods, ranked by which should be financially invested in, based in part on the race and ethnicity makeup of the residents.

Their top-ranked zone was today’s Salisbury Street and Hammond Heights area, where 35.1% of the residents were non-white in 2020. Their lowest-ranked zone, today’s Main South and South Worcester area, had 89.5% of its population identify as non-white in 2020.

Thomas-Bonnick said redlining is still alive and well, even though it has improved in her nearly 30 years in the banking industry. When an entrepreneur is looking for business financing in certain locations, she often sees them turned away.

“Before we even maybe hear the merits of what they're trying to do, we've already decided no, and I don't think it's a conscious decision,” she said.

A 2024 study conducted by researchers from Harvard and Purdue universities found business owners of color had a harder time obtaining loans from the SBA’s Paycheck Protection Program launched in the initial phase of the coronavirus pandemic. The study found Black-owned restaurants are 9.1 percentage points less likely to receive PPP funding than similar white-owned restaurants. For Hispanic-owned restaurants, the difference is 5.6 percentage points.

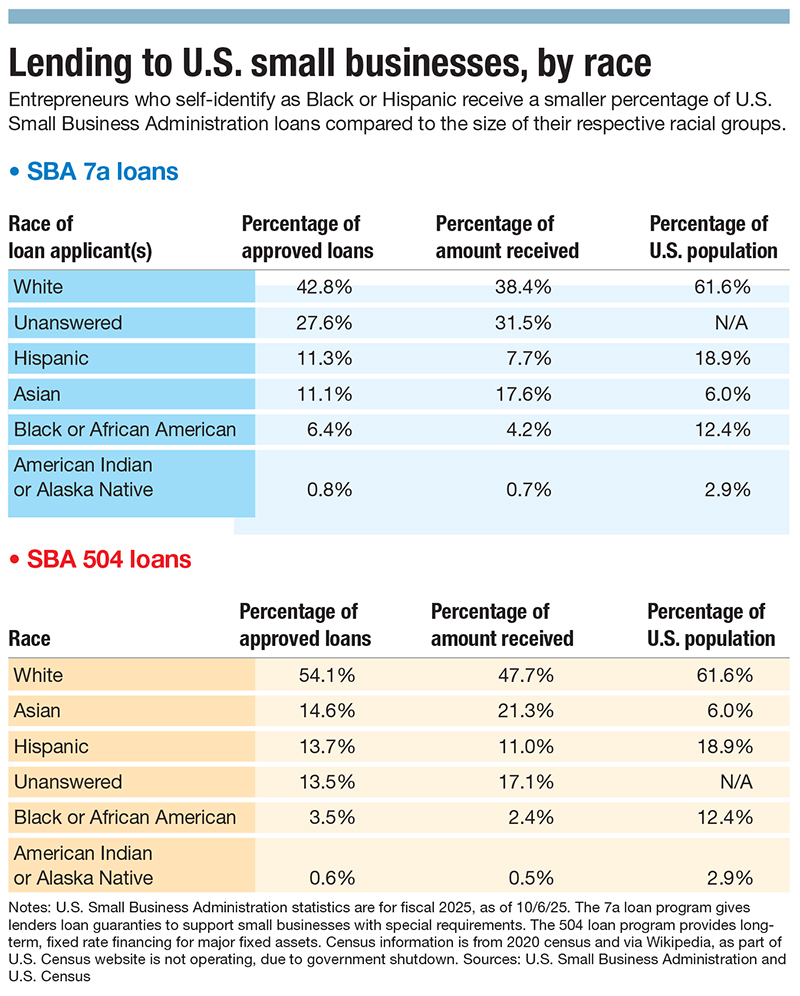

A chart of lending to U.S. small businesses by race

Improving banking access

Marginalized communities tend to have poor credit histories, automatically putting them at a disadvantage as credit scores are the typical litmus test for financial credibility.

A 2022 report by The Urban Institute, a Washington, D.C.-based research institute, reported young adults between 25 and 29 in majority Black communities had a median credit score of 582 while majority Hispanic and majority white communities had median scores of 644 and 687, respectively.

Connecting entrepreneurs to resources can offer them opportunities, like NCMDC did with Clark. This is a cornerstone of good banking, said Lee from St. Mary’s. If a borrower is not yet a fit for a specific institution, it shouldn’t signal the end of the conversation.

“That doesn't mean our journey is over with them. It is our responsibility to make sure that we connect them with the appropriate organization and the entity to help them along in that journey,” she said.

Publicly traded banking institutions can be heavily regulated, and thus can have rigid criteria they need to follow when loaning funds, Lee said.

“When you fall short of the traditional standards, that doesn't mean that another institution may not be more appropriate for you,” said Lee. “If you don't fit the box, we're just going to find another box.”

And a way to effectively do that is by hiring people who look like the communities banks serve, she said.

When Webster Five recognized the demographics of its communities were changing with more immigrants and people of color, the bank made a commitment to diversity, equity, inclusion, and belonging, said Thomas-Bonnick.

It brought on individuals who looked like the community, like her, who work with entrepreneurs of color and ask questions about a low credit score as opposed to just walking away.

Thomas-Bonnick and the sales side of Webster Five have been holding business owner meetings with entrepreneurs of color within Greater Worcester, offering training and gathering feedback about their banking experiences.

Institutions that understand the demographic changes and are willing to identify what different groups need are the ones that have a better chance of succeeding in the future, she said.

“I have to have hope that this country is going to move forward in a manner where it's about a person, about their integrity, about their character, and not about anything else,” she said.

Mica Kanner-Mascolo is a staff writer at Worcester Business Journal, who primarily covers the healthcare and diversity, equity, and inclusion industries.